The vineyards of France and specifically the vineyards of Bordeaux are being watched more and more closely as the ease of gathering social, biological, economic and climatic sources continues to improve. Typically each summer the SAFER (the acronym for Sociétés d’aménagement foncier et d’établissement rural) publish the economic land price data for (Bordeaux) vineyard transactions for the previous year. Historically the reliability of their data was questionable since it was based on averages drawn from each appellation that included both vineyard estates with their adjoining vineyards and individual parcels of vines – these are two distinct asset classes and different markets. Furthermore in small appellations average data was skewed since there were so few transactions that led to results showing significant price swings from one year to the next. Another limitation to their data historically was the fact that their sample was not complete since it only included asset transaction it missed the transactions that were company share transactions.

Today the SAFER’s Bordeaux vineyard information is a lot more reliable and whilst it is not infallible (if you take an average from a data set that is 95% non-chateau vineyards it means that the chateau vineyards will be negatively influenced) it is a very helpful reference. We still note that the SAFER have difficult valuing the marriage value of vineyards and their adjoining buildings and businesses since values for the latter can be structured for tax or strategic purposes thereby skewing values for the vineyards potentially too high or too low. Vineyard transactions are made when a willing buyer and a willing seller agree terms and, as with all purchases, there may be special features or strengths that support premiums or particularly low valuations where weaknesses are outside market norms.

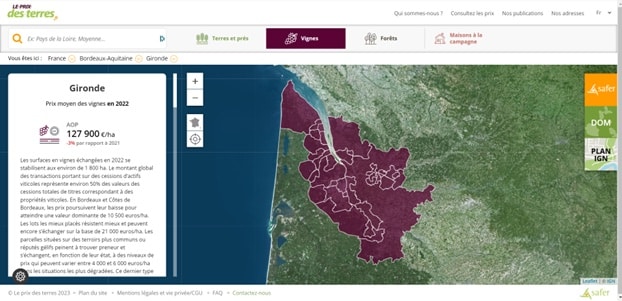

In summary, the SAFER’s data has established that the surface area of vineyards transacted in 2022 was stable compared to recent years with a total at around 1,800 ha of Bordeaux vineyards (we are quoting their numbers but there is an inconsistency we found that we have not been able to clear up with them at the time of writing). Remember this is both standalone vineyards which form the vast majority of trades (about 95%) as well as vineyard estate with their supporting businesses, buildings and chateaux (about 5%). The SAFER report that about 50% of the total value of the transactions were asset transactions while the other half were share transactions via the sale of holding companies.

Bordeaux Superieur and Côtes de Bordeaux

The single largest region of Bordeaux vineyards are those found in Bordeaux Superieur and Côtes de Bordeaux (together making up almost 70% of the vineyard area) where the SAFER report that prices continued to fall in 2022, reaching an average low value of €10,500 euros/ha. The best-placed lots are holding up better, and can still be traded for up to 21,000 euros/ha. Parcels located on less interesting soils, or those with a history of late spring frost, are struggling to find any buyers at all and, depending on their condition, are trading at prices ranging from as low as €4,000 to €6,000 euros/ha in the most run-down situations. In these cases vineyards are being converted to other potentially more profitable farming uses and it is the cost of grubbing-up that keeps prices depressed. The Côtes de Bordeaux appellations are following the same trend as Bordeaux Superieur vineyards. Prices per hectare in the Cadillac, Blaye and Bourg sectors are down by around 15%. A hectare of Cadillac Côtes de Bordeaux is trading at an average of €11,000 euros/ha, while Blaye Côtes de Bordeaux is trading at an average of 13,000 euros/ha and Côtes de Bourg at 16,000 euros/ha. The SAFER go on to report that even Castillon is no longer immune to the downward trend, with values now approaching €20,000 euros/ha, although the best terroirs in Castillon are holding up well, and can still be traded at up to €35,000 euros/ha.

Pessac Leognan, and the Graves

For the first time since the creation of the appellation, prices in Pessac-Léognan have fallen significantly, returning to 2019 levels, with a peak reported at €500,000 euros/ha. In the neighbouring Graves, prices are continuing the decline already seen last year, reaching a value of €27,000 euros/ha. Vineyard parcels located on the best gravel plateaus are still trading at close to €40,000 euros/ha, while the most frost prone sandy terroirs are now struggling to find buyers at €15,000 euros/ha.

The Sauternes, Loupiac and Sainte-Croix-du-Mont

Sauternes continues to have deeply structural challenges as the world has moved away from drinking sweet wines. Nevertheless, prices are stable at around €30,000 euros/ha on average. Sales difficulties for the sweet wines of the right bank are also depressing prices of vineyards in Loupiac and Sainte-Croix-du-Mont. The average value per hectare of these AOP vines follows that of other Bordeaux appellation vineyards, at an average of €10,500 euros/ha.

The Medoc

The SAFER report that in the Médoc, the downward trend that began in 2019 continues. AOC Médoc vines are now trading at an average of €35,000 euros/ha, while the price of AOC Haut-Médoc vines is holding steady at €60,000 euros/ha. Existing players with stable wine distribution are taking advantage of these attractive prices to consolidate their businesses and expand to what can be significant vineyard areas. As in the Haut-Médoc AOC, Listrac (€60,000 euros/ha) and Moulis (€80,000 euros/ha) are holding their own. The prestigious appellations perhaps not surprisingly have not followed the wider trend. Margaux (€1,500,000 euros/ha) and Saint-Julien (€1,800,000 euros/ha) show a certain stability in their average prices, with maximum values close to €2,500,000 euros/ha for Margaux. Pauillac also seems to be entering a phase of stability, with average prices of €3,000,000 euros/ha. In Saint-Estèphe, the prevailing price remains stable at around €550,000 euros/ha, but the gap is widening between the worst terroirs, which trade at €350,000 euros/ha, and the best, which can now reach €1,200,000 euros/ha, or even more when the vines belong to a cru classé estate.

Saint Emilion and the Saint Emilion Satellites

In the Libournais region, the appeal of the Saint-Emilion Appellation remains strong. However, despite the strength of the Saint-Emilion brand name, buyers are increasingly selective when it comes to terroir quality. While the dominant price remains stable at around €300,000 euros/ha, prices in the least sought-after sectors are continuing the downward trend that began in 2021, with values as low as 200,000 euros/ha. Competition for access to the best terroirs remains intense, and prices can reach €3,800,000 euros/ha without classification, and exceed €5,000,000 euros/ha in the case of the sale of well-reputed classified properties. Between these two extremes, each sector is characterized by a unique price level, the analysis of which requires a detailed knowledge of the territory.

Vineyard values in Saint-Emilion’s satellite appellations are generally stagnating. While AOCs renowned for the homogeneity of their terroir, such as Montagne (€120,000 euros/ha) or Saint-Georges (€150,000 euros/ha) are still finding buyers, vines in the Puisseguin or Lussac AOCs, when not benefiting from very favorable situations, are now struggling to buyers, and their prices can fall as low as €55,000 euros/ha.

Prices in the Pomerol vineyards have stabilized at an average of €2,000,000 euros/ha. Here again, location is everything, and the sectors coveted by the appellation’s most prestigious names can reach values in excess of €7,000,000 euros/ha, while the least attractive terroirs maintain a slightly base value of 1,300,000 euros/ha. This threshold is seen by growers wishing to expand their wine range, as the necessary entry ticket to this highly sought after appellation. In Lalande-de-Pomerol, prices have fallen slightly, with prices now around €230,000 euros/ha. The best soils, which are still highly sought-after, are maintaining their prices at around €350,000 euros/ha. In Fronsac, the decline that began in 2020 continues, with price per hectare now down to €22,000 euros/ha. The price of the best terroirs is also falling, but they can still be traded at close to €50,000 euros/ha. Canon-Fronsac is holding steady at around €100,000 euros/ha.

Overall the SAFER’s data is a depressing read – there is no doubt that it is a buyers’ market for all but two of the categories in the Bordeaux vineyard market: the prestigious classified estates and the turnkey hobby vineyards. The SAFER report that overall the market has dropped by an average of 3% with about the same number of vineyard transactions as 2021 – 760 (typically about 95% are just vineyard parcels – ie not chateau vineyards) over 2700 hectares (an increase of 4% on the previous year) which represent about 2.25% of the total 120,000 hectare Bordeaux vineyard surface in production. This number of 2700 hectares is the inconsistency (above we quoted 1800 hectares) but we think that the 1800 hectares number is just vineyards in production and does not include surrounding land that might be sold with the estates recorded.

Written by Michael Baynes – source information SAFER « Le prix des terres 2023 »