: Definition, Operation and Taxation")

Created by a 1970 law designed to preserve the integrity of French agricultural land, the GFV (Groupement Foncier Viticole) has become a discreet wealth‑management vehicle for those who wish to be linked to a wine terroir while entrusting vineyard operations to professionals. Understanding this structure helps explain one of the main ways to access vineyard ownership without purchasing an entire estate.

In Brief

- A GFV is a civil company that owns vineyard land and leases it long‑term to a winegrower.

- Investors own shares in the land, receive rental income (fermage), and may sometimes receive bottles of wine or preferential purchasing terms.

- In 2026, the tax framework is based on three pillars: income‑tax relief under certain conditions, partial IFI exemption, and inheritance/gift‑tax advantages.

- Rental yields are generally between 1.5% and 3.5% per year, potentially supplemented by land appreciation.

- A GFV provides exposure to vineyards without management constraints.

What is a GFV?

A GFV is a civil company whose purpose is to own vineyard real estate: vineyard plots and sometimes buildings and trademarks. Several investors pool capital to acquire land, which is then leased to an operator. The GFV owns the land but does not directly farm it.

The principle is straightforward. Several partners pool their capital to acquire land, then delegate its cultivation. The group’s statutes prohibit it from farming the vines directly: the GFV owns the soil but is never the winegrower. This separation between ownership and the working of the land lies at the very heart of the arrangement, and underpins its tax advantages.

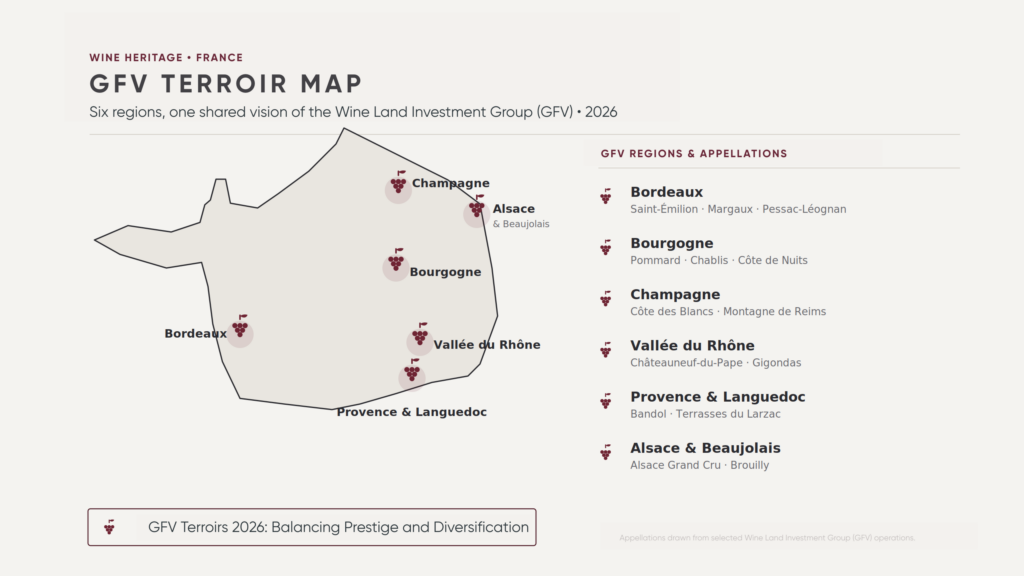

Investing in a GFV therefore means holding a fraction of a vineyard within an appellation, without taking on either the agronomic management or the commercialisation. You become the bearer of a piece of terroir, not its operator. In Bordeaux, these groups sometimes reach first-rank appellations, from Margaux to Pauillac, from Pessac-Léognan to Saint-Émilion, even if availability remains scarce among the most coveted names.

How does a GFV work?

Three types of actors are involved in a wine land investment group (Groupement Foncier Viticole).

The management company structures the group, selects the land, and ensures the smooth running of the operation over time. The shareholders provide the capital and receive in return shares representing ownership of the land. The operator, a winemaker or wine estate, cultivates the vines and produces the wine under a long-term rural lease concluded with the group.

This long-term lease is the cornerstone of the structure. With a minimum duration of eighteen years, it provides the winemaker with the stability needed to carry out patient, long-term work, and grants shareholders the favorable tax regime associated with long-term leasing, in compliance with tenancy laws. In exchange for the use of the land, the operator pays rent (fermage), which is calculated each autumn based on the official rate set by prefectural decree. The shareholder’s income is therefore regulated and predictable, sheltered from the uncertainties of the harvest.

The return from a GFV comes from this rent, generally between 1.5% and 3.5% per year. In addition to this rental income, there are two additional benefits. First, the potential appreciation of the land value, as the reputation of the appellation grows over successive vintages. Second, in-kind benefits: many groups offer shareholders a few bottles from the estate each year, or preferential purchasing conditions. An elegant way to literally taste the fruits of one’s ownership.

Subscription is carried out through the management company, after receiving the key information document. The entry ticket varies from one group to another, starting from a few thousand euros, making vineyard investment accessible well below the cost of purchasing an entire estate.

The tax advantages of a GFV

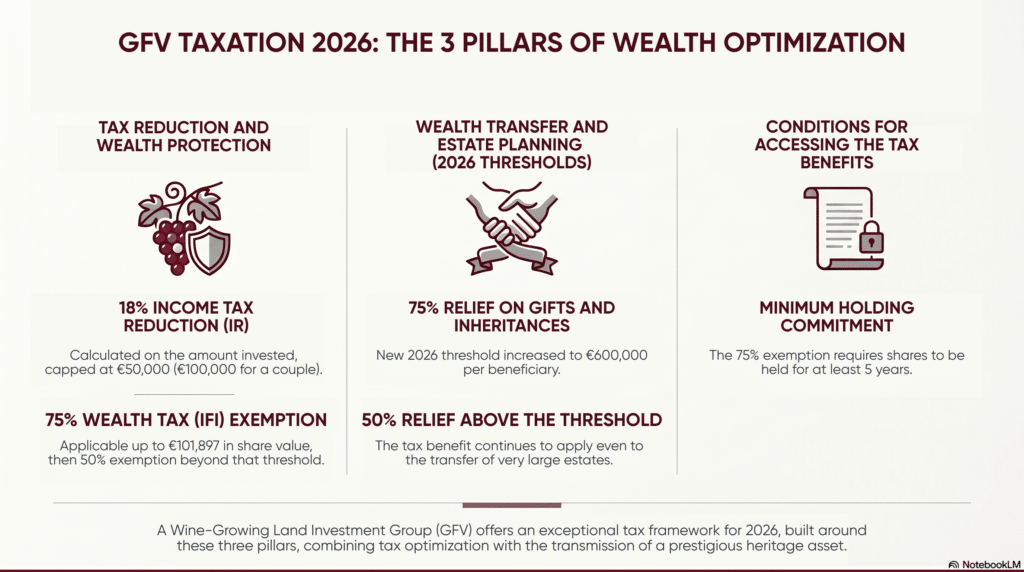

If the Groupement Foncier Viticole (GFV) is appealing, it is above all because of its tax treatment, among the most favorable in French law for a tangible asset. In 2026, its attractiveness is based on three pillars, subject to certain conditions:

- An income tax reduction of 18% of the amount invested, for subscriptions eligible under the scheme for investment in the capital of small and medium-sized enterprises.

- Partial exemption from the IFI (real estate wealth tax), amounting to 75% of the value of the shares up to €101,897.

- A transfer allowance of 75% of the value transferred, up to €600,000, in both gifts and inheritances.

Let’s go over each of these levers

Pillar 1: the income tax reduction

Some share subscriptions qualify for an income tax reduction of 18% of the amount invested, under the scheme for subscribing to the capital of small and medium-sized enterprises. The ceiling on eligible contributions is €50,000 for a single person and €100,000 for a couple: an investment of €50,000 can therefore represent up to €9,000 in tax savings. However, this benefit is not automatic. It depends on the eligibility of the group, whereas the IFI relief and the inheritance/gift allowance form the core of the scheme.

Pillar 2: partial exemption from the IFI

Shares in a GFV benefit from an exemption from the real estate wealth tax (IFI) of up to 75% of their value, up to a limit of €101,897, and then 50% beyond that threshold. This benefit applies to shares held for more than two years, provided that the land is leased under a long-term lease. For assets subject to the IFI, the tax relief is significant.

Pillar 3: a tool for wealth transfer

This is probably the area where a GFV expresses its full value. Since the 2025 finance law, gifts and inheritances are exempt from transfer duties up to 75% of the value transferred, up to €600,000, subject to a five-year holding commitment for the shares. This threshold was previously set at €300,000. For the largest estates, the 75% exemption can extend up to €20 million, provided the holding commitment is extended to eighteen years. Beyond these limits, the allowance remains 50%.

This benefit applies only to the portion of shares corresponding to land leased on a long-term basis, and requires that the shares have been held for more than two years by the donor. Passing on a vineyard to one’s children thus becomes significantly less costly than a conventional real estate transfer.

Beyond the three pillars: income and capital gains

The rent received is treated as property income: the micro-foncier regime provides a 30% allowance as long as this income does not exceed €15,000 per year. Upon resale, the shares are subject to the regime for private real estate capital gains, with exemption from income tax after twenty-two years of ownership, and from social security contributions after thirty years.

GFV or direct acquisition of an estate?

The Groupement Foncier Viticole and the purchase of a wine estate meet two distinct aspirations. One offers measured exposure to vineyard land; the other provides full and complete ownership of a place.

| Criteria | Groupement foncier viticole | Direct acquisition of a wine estate |

| Nature of the asset | Shares in a civil company | Full ownership |

| Entry ticket | From a few thousand euros | Several hundred thousand to several million euros |

| Management | Delegated to an operator | Controlled by the owner |

| Control over the estate | None | Total |

| Lifestyle aspect | Symbolic | Fully experienced |

| Liquidity | Limited, exit uncertain | Market for luxury properties |

| Taxation | Reduced IFI and inheritance taxation | Depends on the structure chosen |

The GFV suits those who wish to put down roots in a terroir with flexibility and without the constraints of running an estate. Acquiring a property speaks to those who want more: a château, a cellar, a landscape, a history to carry and, at times, to pass on. This path opens access to working wine estates, vineyards for sale or simply vine parcels to cultivate. It is precisely this support, from the search for an exceptional property through to its transmission, that defines the craft of Vineyards-Bordeaux.

How do you choose a GFV?

First, the reputation of the appellation: a recognised AOC helps protect land value and the stability of the rent (fermage). Second, the strength of the operator, as the yield depends on their ability to sell wine over time. Finally, the age and track record of the group, which reveal the quality of its management, ideally over five to ten years. Some degree of diversification, whether geographical or across estates, also helps mitigate the risk associated with a single terroir.

Limitations and points of caution

Clear-eyed realism is essential. A GFV is a long-term investment, with a recommended horizon of more than ten years, and it remains relatively illiquid: resale of shares takes place on the secondary market organised by the management company or through an over-the-counter transfer, and only succeeds if a counterparty is found. Entry fees, often between 5% and 10%, weigh on initial returns. Capital is not guaranteed, as the value of the land may fall as well as rise depending on the appellations. The rental yield remains modest, with the main appeal lying in the tax framework and the asset’s patrimonial nature. Finally, the tax exemptions described depend on strict compliance with specific conditions, the breach of which leads to their reversal.

Conclusion

The Groupement Foncier Viticole occupies a unique place in the French wealth landscape: that of a tangible asset, rooted in its terroir, benefiting from a rare tax regime in terms of IFI and wealth transfer. It allows one to approach viticulture without bearing its operational burdens, and to prepare the transfer of assets under favourable conditions. However, for those who dream of owning an entire estate, walking its rows, and writing its next chapter, a GFV remains a step, never an end in itself. Full ownership of an exceptional vineyard belongs to another ambition, and requires a level of support to match. To discuss this further, the team at Vineyards-Bordeaux is at your disposal.

In brief

- A GFV is a civil company that owns vineyard land leased to an operator under a long-term lease.

- The shareholder receives rent, benefits from tax advantages, and sometimes receives an in-kind share.

- Three tax pillars in 2026: an 18% income tax reduction under certain conditions, a 75% IFI exemption up to €101,897, and a 75% allowance on transfers up to €600,000.

- A long-term and illiquid investment, a GFV is mainly valued for its wealth-building and tax advantages.

- Direct acquisition of an estate remains the path for those who want full ownership of a vineyard.

Q&A

It is a civil company that brings together shareholders to own vineyard land, which is then leased to a winemaker. The shareholder owns shares in the land, without personally operating the vineyard.

It varies depending on the group, and often starts at a few thousand euros, making vineyard investment accessible at a level far below the price of a full estate.

An income tax reduction of 18% of the amount invested, subject to eligibility conditions; a partial exemption from the IFI (real estate wealth tax) of 75% up to €101,897 in shares; and a 75% exemption from gift or inheritance tax up to €600,000, subject to a long-term lease and holding commitment.

Under certain conditions, yes. A tax reduction of 18% of the amount invested may apply to eligible subscriptions under the scheme for investing in the capital of small and medium-sized enterprises, up to a limit of €50,000 for a single person and €100,000 for a couple. This benefit is not automatic and depends on the structure of the group; it differs from the IFI exemption and the transfer allowance, which form the core of the GFV scheme.

The rent (fermage) provides an annual income of around 1.5% to 3.5%, to which potential land value appreciation and an in-kind share may be added. The investment is valued as much for its tax framework as for its current yield.

No. The statutes prohibit the group from directly operating the land. To run an estate and control every decision, direct acquisition of a property is required.

No. The value of the shares can go up or down, and resale depends on demand. A GFV is a long-term commitment.

This article is for informational purposes only and does not constitute personalized tax or legal advice. Each wealth situation requires the opinion of a notary or a wealth management advisor.

Sources

- Finance Act for 2025, Article 70, raising the thresholds for exemption from gift and inheritance taxes on rural property and shares in landholding groups.

- Official Public Finance Bulletin (BOFiP), partial exemption for shares in agricultural and wine landholding groups, Article 793 bis of the French General Tax Code.

- French General Tax Code, Article 199 terdecies-0 A, tax reduction for subscriptions to the capital of small and medium-sized enterprises.

- Rural and Maritime Fishing Code, Articles L322-1 to L322-23 relating to agricultural and wine landholding groups.

- Service-public.fr and impots.gouv.fr, rules governing the real estate wealth tax (IFI) and property income taxation.

- Meilleurtaux Placement, “Understanding the Groupement Foncier Viticole (GFV)”.

- GroupementFoncierViticole.com, GFV operation and taxation.

- Haussmann Patrimoine, definition and taxation of GFV.