Bordeaux Vineyard Valuation Data sources

Each year during the summer season the SAFER release their interpretation of the previous year’s vineyard activities. If you are new to Bordeaux vineyards, then you may be asking what does the SAFER stand for? “Les Sociétés d’Aménagement Foncier et d’Etablissement Rural” – broadly this would translate as the French Land Agency. They are privately funded from fees taken at the time that agricultural transactions are completed but, they are publicly mandated making them a kind of quasi-public institution. In France they are the best source of data for the overall agricultural market and as a subset of this of course vineyards and specifically Bordeaux vineyard valuations can be analysed.

There are two other sources of data: the press, for example Decanter, Wine Spectator and the local French press such as the Sud Ouest newspaper and then the tiny group of winery transaction specialists who are managing these vineyard transactions of which Vineyards-Bordeaux is one.

The Reliability of the data

We are going to focus on the SAFER’s data since it is the closest thing we have to a universal view of the whole market. But, it is not perfect and definitions for what constitutes a vineyard and even a vineyard sale do vary. For example, prior to January 2017 the SAFER were not involved in any share transactions (where the company shares of a winery company are sold) – this had the effect of skewing data since the most valuable estates were uniquely sold as share transactions. Since January 2017 the SAFER are involved in share transactions but only if 100% of the shares are being sold. For discretion purposes therefore, we sometimes see deals that are reduced down under 100% of the shares to maintain privacy and avoid the SAFER involvement. These reasons amongst others mean that we still do not have a complete and fully reliable data picture. Finally, we must remember that the SAFER are primarily focused on sales of parcels of land. For example, a normal year might see 700 Bordeaux vineyard transactions that are just land parcels (just vines on land) while the market for chateaux-vineyard transactions would be about 30 sales making the total market 730.

Clearly however, you can see that if average prices within appellations are being drawn from this data set they will be heavily skewed to the parcel transactions which form over 95% of all transactions. It means that journalists and those unfamiliar with the Bordeaux vineyard market can be misled in reading data drawn from averages published by the SAFER because the data is sourced from two completely different products: 1) Chateaux-vineyards including “hobby vineyards” (with trademarks, buildings, business goodwill, staff, equipment etc) and 2) parcels of vines with nothing but plants in fields. Nevertheless, the chateaux-vineyard transactions tend to be much bigger by land area. For example, in 2017 this group was almost 25% of the vineyard land area sold even though it was a much small number of transactions than the parcel only sales.

The 2017 Vineyard Market

2017 was a very strong year for the number of Chateaux-vineyard (i.e. excluding parcels only as explained above) transactions and the strongest since 2013 which was the high point for the Chinese vineyard purchase activity in Bordeaux. However, the total area of vineyards by hectares sold was only up very slightly from 694.36 hectares to 702.67 hectares. What is clear from analysing the data since 2012 is that large estates were being traded in 2012, 2013 and 2014 (this is what the Chinese investors were targeting) and then in 2016 and 2017 we see smaller total hectares being traded but the value of these transactions being higher. In other words, the market is getting stronger in the prestigious appellations as demand for the top brands and chateaux forms the focus of investor interest.

In a “normal” Bordeaux transaction year we see about 30 chateaux-vineyards changing hands. For example, in 2014 it was 30, in 2015 it was 25 and in 2016 it was 28. But in 2017 this jumped significantly to 48 total transactions for chateaux-vineyards across all Bordeaux appellations. What was also interesting was that the value of these 48 Bordeaux vineyard transactions also increased from an average of €4.5m in 2016 to an average of €6.6m in 2017 – the average for the past six years is just under €5.4m. However inside these averages there are three vineyard markets:

- The ultra valuable trophy estates such as Chateau Troplong Mondot – the Saint Emilion Premier Grand Cru Classé sold to to the French insurance company SCOR Group for €178m in 2017

- The large commercial vineyards such as Chateau Bel Air – Cotes de Bordeaux Castillon (pictured below) sold to Chinese group – Golden Fields

- The Hobby Vineyards such as Chateau Prieuré St Anne (pictured above) – sold to private individuals from Belgium

It is also interesting to note that of the 48 transactions in 2017 there is still a sizeable percentage (33%) that are being sold to Chinese investors. This certainly echoes our experience at Vineyards-Bordeaux where Chinese interest remains strong despite Chinese international capital restrictions.

Valuation of vineyard land and Trademark

Last week Petrus announced the sale of a 20% stake for €200,000,000 Euros to Colombian billionaire Alejandro Santo Domingo. This stake values the estate of 11.4ha at over €87 million per hectare. Apart from the eye watering numbers and the glamourous nature of the transaction why is this an important part of any analysis of Bordeaux vineyard valuations. It demonstrates the immense impact of two factors: the first is the power of the trademark, arguably the Petrus trademark is about €85 million per hectare and secondly, but not unrelated, the market value of the wine produced at that chateau. The release price has been around 850€ per bottle so let’s say the average selling price is 1500€ (now trading 2017 for 2300€ per bottle). Trademarks tend to have significant effect on trophy assets, less effect but still important for commercial vineyards and much less effect for the “Hobby Vineyards” market.

2018 and beyond

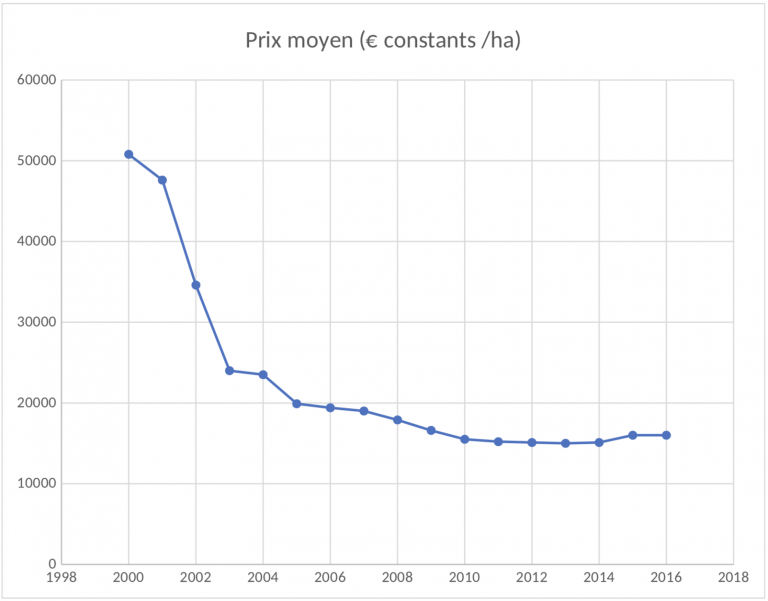

Like all valuations for any asset, there is no precise science to it. The SAFER’s annual numbers form one important part of the market understanding – perhaps more the trends. If the trend of the largest part of the Bordeaux market (about 70% is made up of Bordeaux Superieur and the Cotes de Bordeaux which together are very close in value) the graph below demonstrates that the market cycle is stable. At Vineyards-Bordeaux we are managing transactions of market leaders in the Bordeaux Superieur and Cotes de Bordeaux that are already matching the average price per hectare levels achieved 18 years ago (over 50,000 Euros/hectare). If the market leaders are a judge of what is coming next, then it is reasonable to assume that the cycle will return to where it was 18 years ago.

The market trend therefore is positive but what is clear is that with the prestigious appellations now getting new record prices it is logical that the wider appellations will follow both for commercial vineyards as well as the hobby vineyards.

Written by Michael Baynes, co-founder of Vineyards-Bordeaux – specialists in M & A (Mergers and Acquisitions) work and vineyard / winery transactions and affiliates of Christie’s International Real Estate.

If you are interested in investing in a vineyard in Bordeaux – or any other region of France – or you have a vineyard for sale, please contact michael@vineyardsbordeaux.com